Page 115 - ICD-AR22-English

P. 115

Notes to the Separate Financial Statements

FOR THE YEAR ENDED 31 DECEMBER 2022

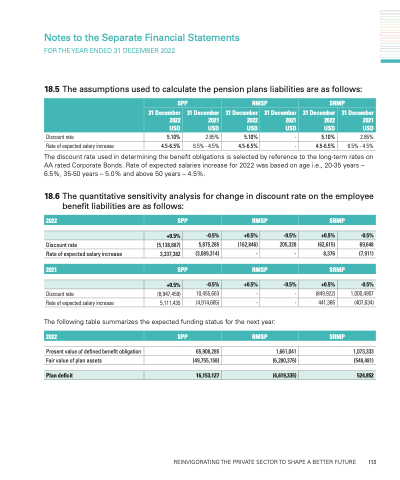

18.5 The assumptions used to calculate the pension plans liabilities are as follows:

Discount rate 5.10% 2.85% 5.10% - 5.10% 2.85%

Rate of expected salary increase 4.5-6.5% 6.5% - 4.5% 4.5-6.5% - 4.5-6.5% 6.5% - 4.5%

The discount rate used in determining the benefit obligations is selected by reference to the long-term rates on AA rated Corporate Bonds. Rate of expected salaries increase for 2022 was based on age i.e., 20-35 years – 6.5%, 35-50 years – 5.0% and above 50 years – 4.5%.

18.6 The quantitative sensitivity analysis for change in discount rate on the employee benefit liabilities are as follows:

SPP

RMSP

SRMP

31 December 2022 USD

31 December 2021 USD

31 December 2022 USD

31 December 2021 USD

31 December 2022 USD

31 December 2021 USD

2022

SPP

RMSP

SRMP

+0.5%

-0.5%

+0.5%

-0.5%

+0.5%

-0.5%

Discount rate

Rate of expected salary increase

Discount rate

Rate of expected salary increase

(5,138,887) 3,337,382

(8,947,459) 5,111,435

5,875,285 (3,089,314)

10,455,663 (4,914,665)

(162,846) 205,328 (62,615) 69,648

- - 8,376 (7,911)

- - (849,922) 1,000,4907

- - 441,366 (407,634)

2021

SPP

RMSP

SRMP

+0.5%

-0.5%

+0.5%

-0.5%

+0.5%

-0.5%

The following table summarizes the expected funding status for the next year:

2022

SPP

RMSP

SRMP

Present value of defined benefit obligation

65,908,285

1,661,041

1,073,333

Fair value of plan assets

(49,755,158)

(6,280,376)

(548,481)

Plan deficit

16,153,127

(4,619,335)

524,852

REINVIGORATING THE PRIVATE SECTOR TO SHAPE A BETTER FUTURE 113